Menu

Trading Justice Newsletter

Trading Justice Newsletter

The 28th day of June of that year would turn out to be decisive for the entire humanity. An ambush was set. One person should be killed. One single outcome was desired.

The stage is set, the crime is perpetrated as planned. The goal? Never reached. Instead, entire nations deteriorated into one of the deadliest conflicts in human history. Hell was concrete. The Four Horsemen were unleashed.

–The person: Gavrilo Princip.

–The victim: Archduke Franz Ferdinand of Austria.

–The place: Sarajevo.

–The (unintended) aftermath: World War I.

–The casualties: About 40 million people, including military and civilians.

–The social economic and geopolitical impacts: Unmeasurable.

Welcome to the July 2019 edition of the Trading Justice newsletter. In this edition, we will be talking about the Extremistan, the world of extreme events.

“That’s just the way it is

Some things will never change

That’s just the way it is”

Humans are complex and so is their History. Complex, organic minds create complex, organic systems that, in turn, set the stage for black swans appearances. Once they appear, things are never the same. Looking forward, unpredictable. In hindsight, they were always there.

Your life, if you look back and start to connect the dots from a certain point in time until today, until now, where you are, you are going to witness the staggering number of “single” events that changed your entire course forever. One “yes” or one “no”, or even one “maybe”, for that matter. Everything changed, forever, a whole new path blossomed and bloomed while all the others withered, faded to black, for better or for worse.

Why Extremistan?

Because that’s the Universe, that’s the Nature, that’s us, that’s life, and that’s the financial markets, by consequence. We are traders and investors and this is our world. That’s just the way it is.

The Extremistan is absolutely no stranger for the readers of the Trading Justice Newsletter, neither for the readers of the famous Tackle Today blog.

We gave special attention to the extreme world of financials in the Holy Trinity of Trading series, published from February to April 2019, precisely on the second part, where we talked about position sizing.

We always start to talk about the Extremistan with the same approach as Nassim Taleb’s, suggesting a very doable exercise:

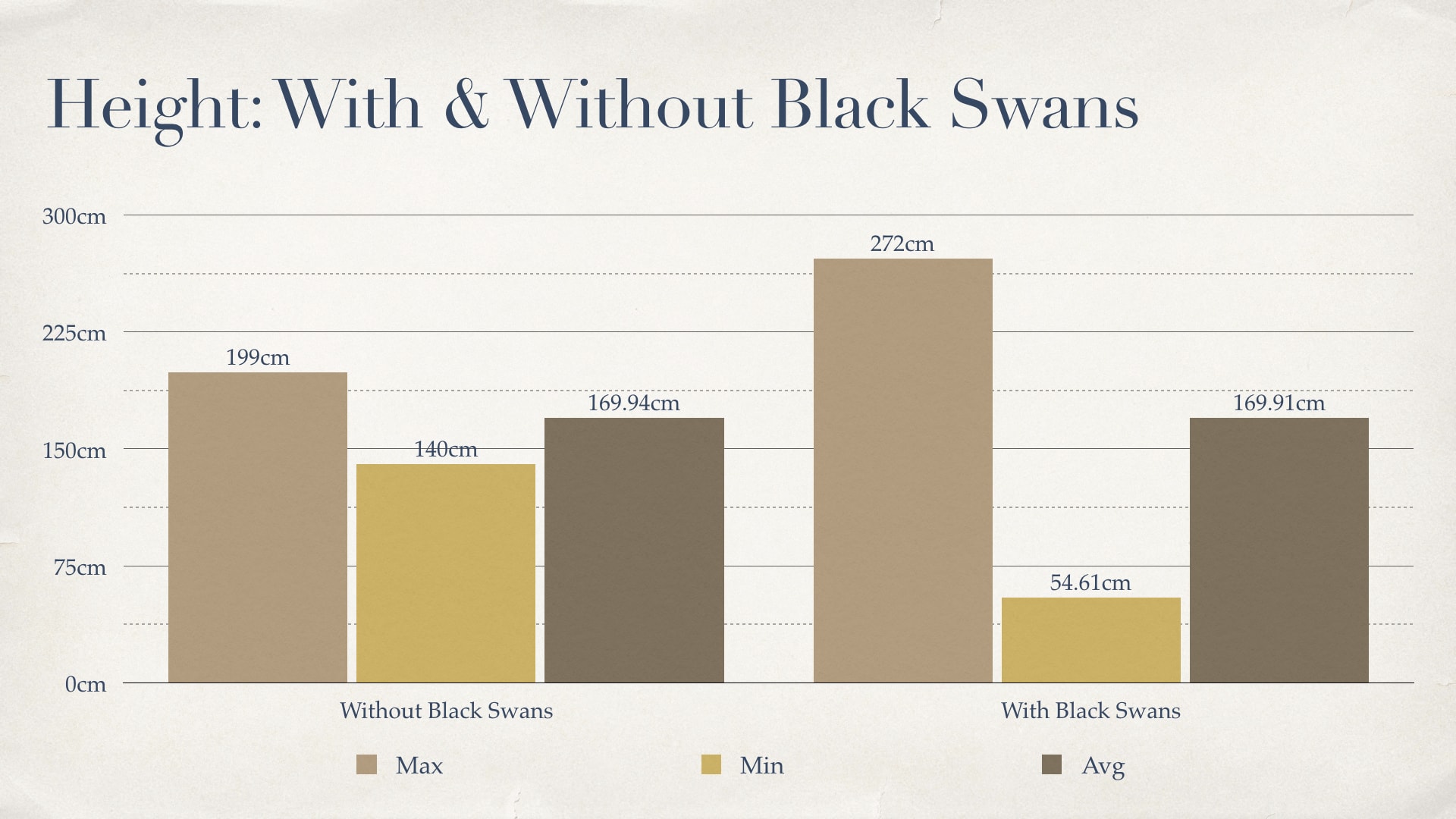

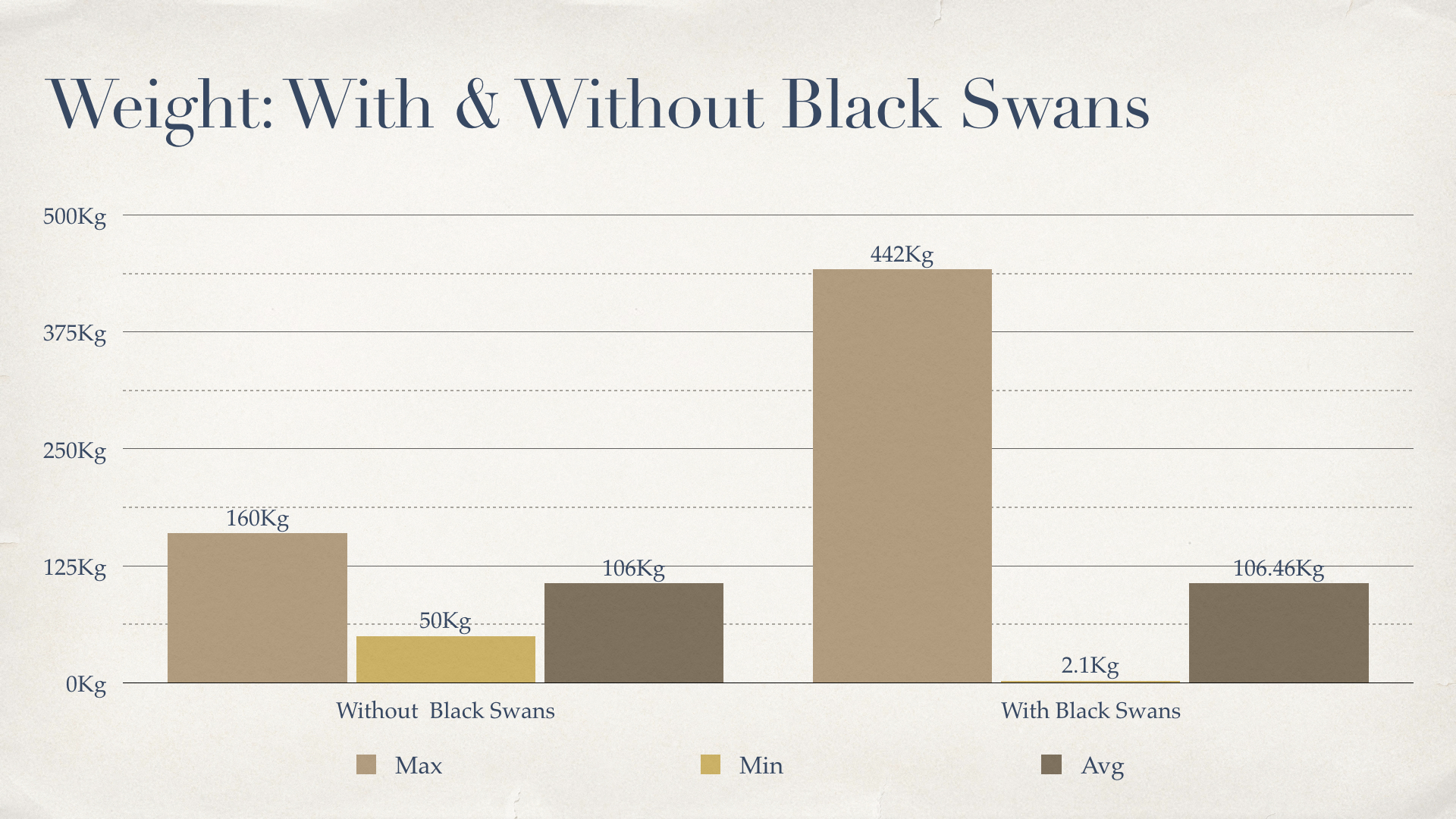

Get 1,000 people and measure their height and weight. Get the max and min values and then the average. Add to this pool the tallest and shortest individuals you can find. Remake the calculations. Add to this pool the heaviest and the lightest people you can find. Remake the calculations.

This time, instead of guessing what you are going to find out data wise, let us grab some data from kaggle.com and work on this experiment together. Here are the max value, min value and the average calculated from a sample containing weight and height from 500 individuals.

It didn’t even scratch the surface as you can already tell by the average, even on such a small sample (500 individuals). Both moved decimals when confronted with extreme attributes.

It should be no surprise. Mediocristan is a boring world. Nothing is scalable and everything is constrained. In our case, constrained by the limits of biological variation. In such an orderly world, even the most extreme value does not affect significantly the entire sample. Black Swans are rare species in these bell curve-shaped lands and when they occur, no one cares; their overall impact is not that significant relative to the total.

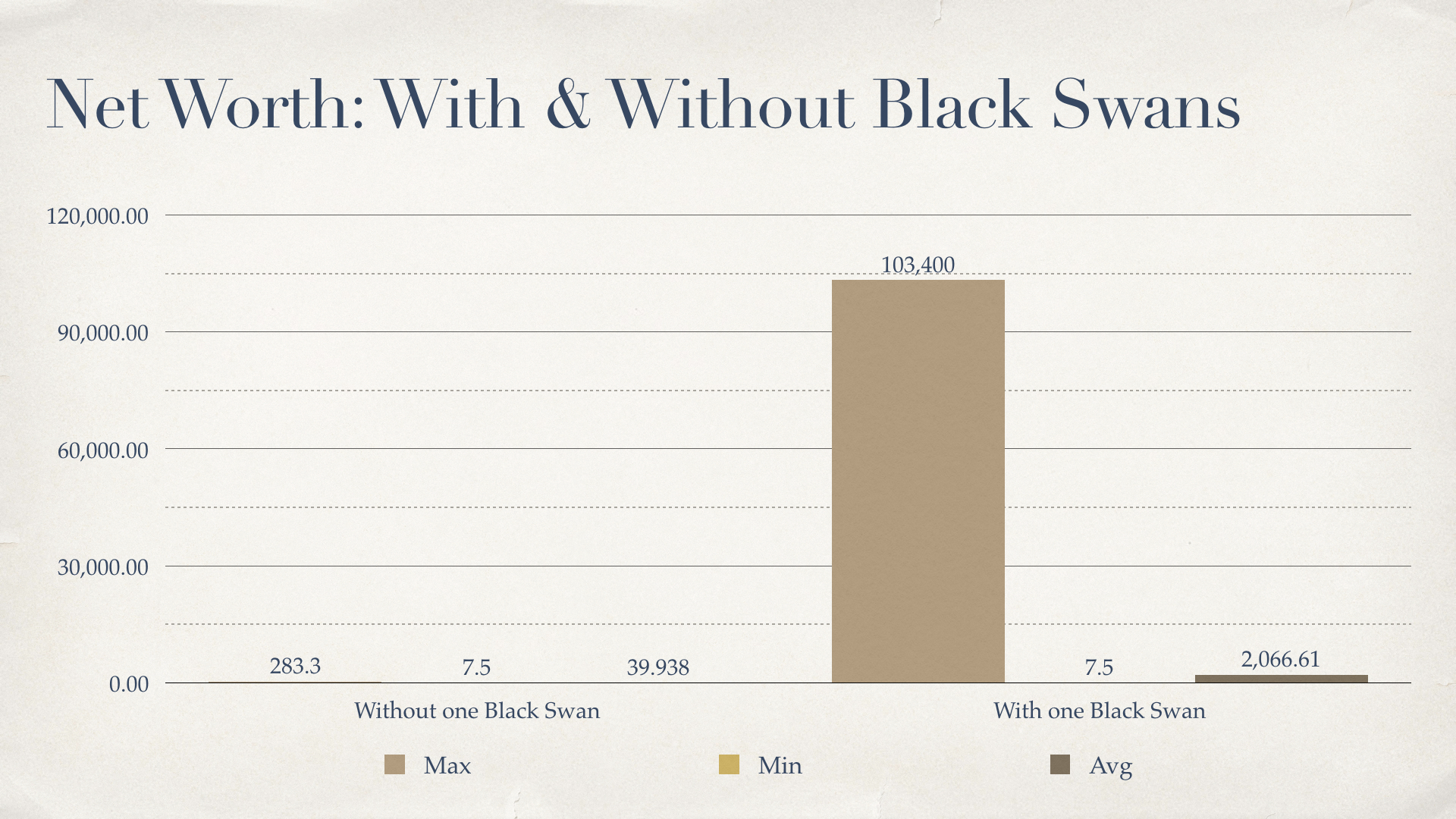

Now, the net worth.

Get 1,000 people and calculate their net worth. Get the maximum and minimum values and calculate the average. Now add to the pool only one individual: Bill Gates.

Let me go rogue on this one if that’s OK with you. Instead of retrieving the net worth of ordinary human beings, why not retrieve the net worth from wealthy people? The list of current members of the United States Congress ranked by wealth sounds very appropriate for this newsletter. Instead of recovering the entire list of 530 members, just the top 50 will help make the case (the data is publicly available at rollcall.com).

One outlier accounts for the whole sample. How much of the total wealth does Mr. Gates represent? 98.10% to be more precise.

This case is definitely part of the Extremistan World, the land of no constraints and full scalability. These terrains are not a nice fit for regular, boring, common sense statistical models. We’re are in Taleb’s Fourth Quadrant, a place where we think we can apply those simple, nauseating methods to calculate the probability of events. There are places where statistics works well and others where it becomes questionable or completely unreliable. Here we are.

The financial markets belong to the Extremistan. A land ruled by randomness and where statistics can fool you. Millions of individuals buying and selling every day, making decisions based on cognitive biases. On such an extreme world, one single day can determine the profits or losses of a whole month. One month can account for the profits or losses of your entire year, as we are going to show you in a little bit.

If simple statistical methods are unreliable here and knowledge is questionable or no longer valid, we should have strict policy rules on how to conduct ourselves, what to do and what to avoid. The decision-making process in such a complex environment can be very difficult due to the impossibility to make reliable inferences from sample data in, in contrast to that of the Mediocristan.

The bulls represent the frenzy in the markets. When prices start to run, people jump into the wagon and buy too. In a bull market, everyone is a genius.

In the Extremistan, the bulls count much more than the bears. Such a statement could be a surprising one to most people. By saying that the financial markets belong to the Extremistan world, it becomes perfectly comprehensible that the bears come into mind first, due to the relationship people trace between the idea of an extreme world and catastrophic events.

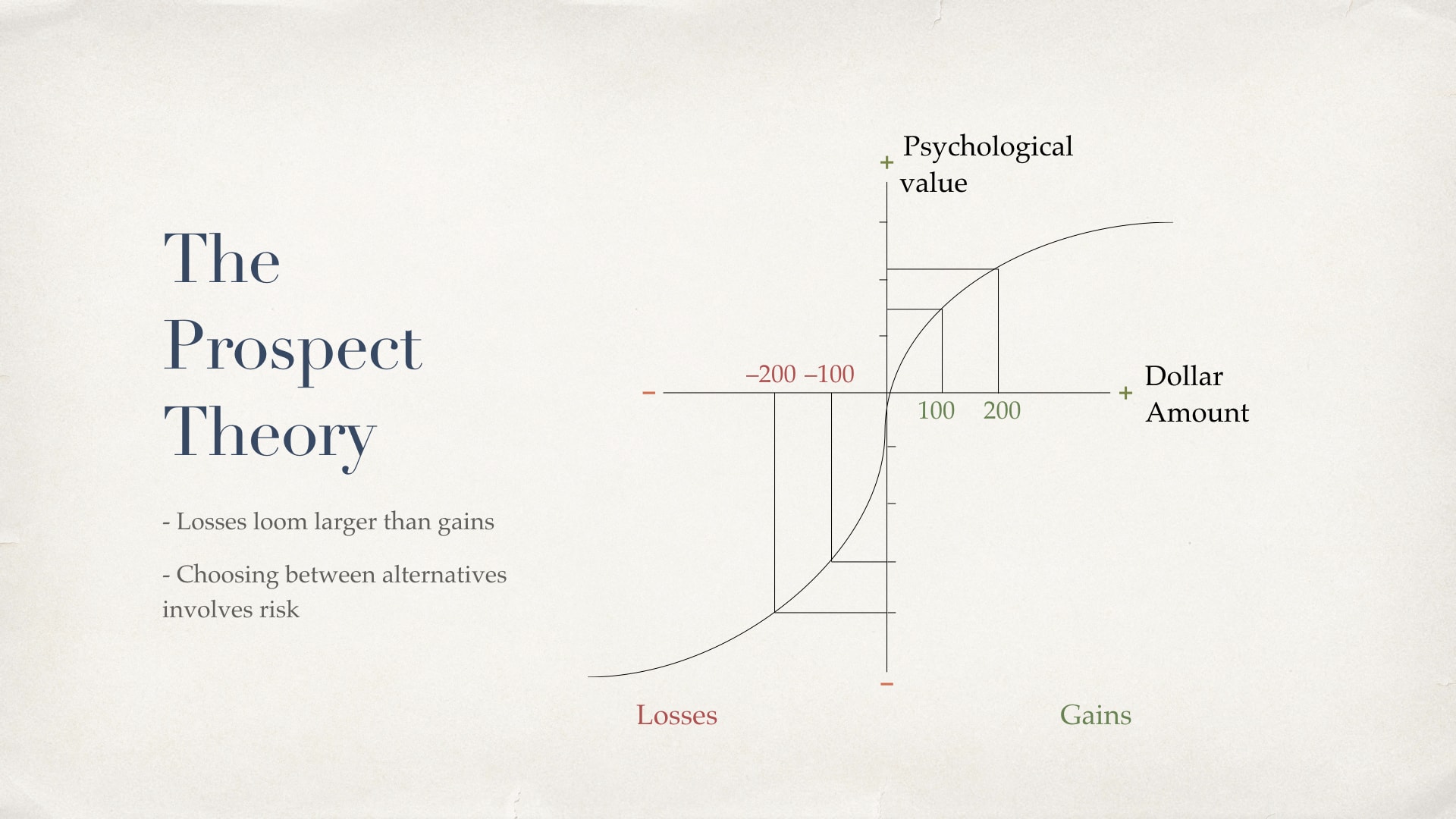

One feasible explanation to this instant connection is the Loss Aversion bias, perfectly encapsulated in Kahneman & Tversky’ expression “losses loom larger than gains”.

According to this theory, it is thought that the pain of losing is psychologically about twice as powerful as the pleasure of gaining. Under such perspective, losing –$2,000 will probably cause more pain and distress than a +$2,000 profit will cause joy and happiness. The two sides of this coin are not the same. The –$2,000 loss will feel like –$4,000 and will likely traumatize the trader.

For the sake of the argument, we ran a simple experiment that will show you that the bulls shaped the Extremistan in the last 20 years and no one seems to care; they will only talk about the crash during the subprime crisis.

We grabbed the S&P 500 daily returns from June 29th, 1999, till June 28th, 2019, on a total of 5,054 working days (7,304 total calendar days minus 2,250 days skipped: 1,043 Saturdays, 1,043 Sundays and 164 holidays). In 20 years, the total return was 117.67%. That is some 5.88% annual return. Sounds good? Obviously not. Educated traders can generate much more return than that.

Now the core question: What happens to this return if we take the top 10 days out of the sampled data? In other words, what happens if we ERASE FROM HISTORY the largest daily point gains like they didn’t even exist? Here’s the past data we are going to erase from History:

| Rank | Date | Net change (Points) |

| 1 | 2018-12-26 | 116.6 |

| 2 | 2008-10-13 | 104.14 |

| 3 | 2008-10-28 | 91.59 |

| 4 | 2019-01-04 | 84.05 |

| 5 | 2015-08-26 | 72.9 |

| 6 | 2018-03-26 | 70.29 |

| 7 | 2000-03-16 | 66.32 |

| 8 | 2001-01-03 | 64.29 |

| 9 | 2018-11-28 | 61.65 |

| 10 | 2008-09-30 | 59.97 |

I bet you would say “Meh, nothing will happen. What are 10 days in 5,054, anyway?”

I gotta admit you have a good point: ten working days represent a mere 0.19% in about 5,000 working days. Staying out of anything that represents only 0.19% of whatever, will never hurt.

However …

You are bluntly wrong. In 20 years, the total return without the top 10 working days was 28.10%. That is ≈ 4.19 times LESS return just because of those 10 miserable days you’ve missed. Take 28.10% and divide it by 20 and you got 1.40% annual return.

That is why the name of this territory is Extremistan. You can be easily fooled by common sense, that innocent assumption that 0.19% of a sample would never, ever, determine the bulk of the results. But it does. Just like the net worth example briefly explained at the beginning of this edition. In the Extremistan, one day can determine the profit or loss of a whole month. One month can account for the profits or losses of your entire year. Ten days can account for most of the profits in two decades.

The best takeaway from this tiny experiment is: you don’t need to follow Red Bull’s website to find the best waves to surf in the entire planet. The Extremistan of the Bulls is the wave to ride. A few days out of the Sea of Bulls and you don’t get as near as much a return you deserve.

Get exposure to the bulls. If, for example, a broad index, like the S&P 500, falls hard, you buy it, because it is not a matter of IF it is going to recover, but WHEN.

Welcome to the Extremistan of the Bulls.

The late 80s and early 90s were prolific in terms of TV commercials that, at some point, a “BUT WAIT, THERE IS MORE!” would be thrown at you. That awkward situation where you would get an electronic Sudoku gadget while buying a kitchen knife set.

The Extremistan of the Bulls has something more to offer to you.

In the previous section, we showed you what it was like to be out of the top ten days of the S&P 500 from 1999 to 2019. To accomplish the task we erased from History the largest daily point gains like they didn’t even exist.

Now, pay attention: we said “daily points”.

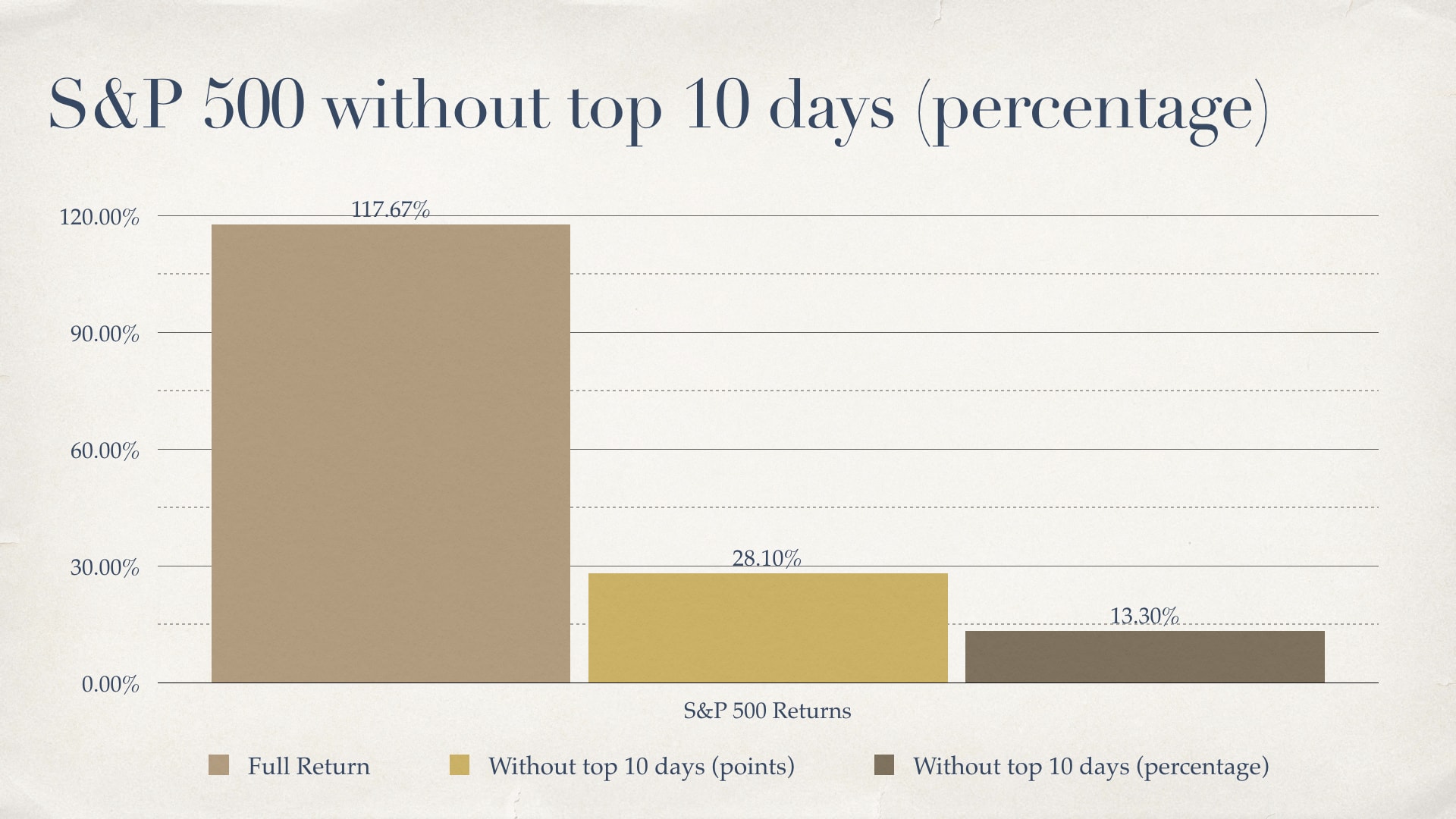

What if we use the same timeframe but instead of erasing the largest daily *point* gains we erase the largest daily *percentage* changes?

I bet you would say: “Our total return already got pulverized. It can’t go any lower.”

Actually, it can. Here’s the data:

| Rank | Date | Net Change (Percentage) |

| 1 | 2008-10-13 | 11.58 |

| 2 | 2008-10-28 | 10.79 |

| 3 | 2009-03-23 | 7.07 |

| 4 | 2008-11-13 | 6.92 |

| 5 | 2008-11-24 | 6.47 |

| 6 | 2008-09-30 | 5.42 |

| 7 | 2001-01-03 | 5.01 |

| 8 | 2018-12-26 | 4.96 |

| 9 | 2000-03-16 | 4.76 |

| 10 | 2011-08-09 | 4.74 |

In 20 years, the return without the top 10 largest *percentage* changes was 13.30%. That is ≈ 8.85 times LESS than the total 117.67% return of the S&P just because of 10 miserable days, being 5 of them in 2008 alone. What a year!

To put this type of return into (a disgraceful) perspective, divide it by 20 years and you get an average of 0.66% annual return.

You would be more profitable selling blueberry muffins on a street fair.

Markets are a huge money transfer machine and the bears are the proof to that affirmation. They are the ones that define and shape the financial markets, testing people’s convictions all the time until the weak ones give up.

A quick search on the web can return quite an impressive amount of theory about the bear’s sense of smell. It is about 7 times better than a blood hound’s and 2,100 times better than a human. A bear’s sense of smell is so acute that they can detect animal carcasses upwind and from a distance of 20 miles away.

The internet is filled with wisdom. You don’t need to be a nerd or a geek to find out that there is a guide, a checklist or a Q&A for almost anything.

Almost.

The search for “How To Be The Perfect Bear Prey and Professionally Fail in the Stock Market” returned zero results. That’s not fair. Failing in the stock markets is the rule. Succeeding is the exception. I think Tackle Trading should be the first company to tap into this field.

With that said, let’s fill that gap with an honest attempt to answer this question. Here’s our recipe for “How To Be The Perfect Bear Prey and Professionally Fail in the Stock Market”.

Not the definitive recipe for disaster, but we guarantee that if you follow every step, your failure is going to be EPIC and the bears will tear you into little pieces. Good luck.

Those of us who have lived through market corrections, know that the statement “Markets take the stairs up and the elevator down.” is 101% true. Even if you are a newbie in the realms of trading, just go back some ten years on the S&P chart to see how bad corrections are compared to rallies. From this perspective, taking the elevator would be too classy; most probably it’s a jump out of the window.

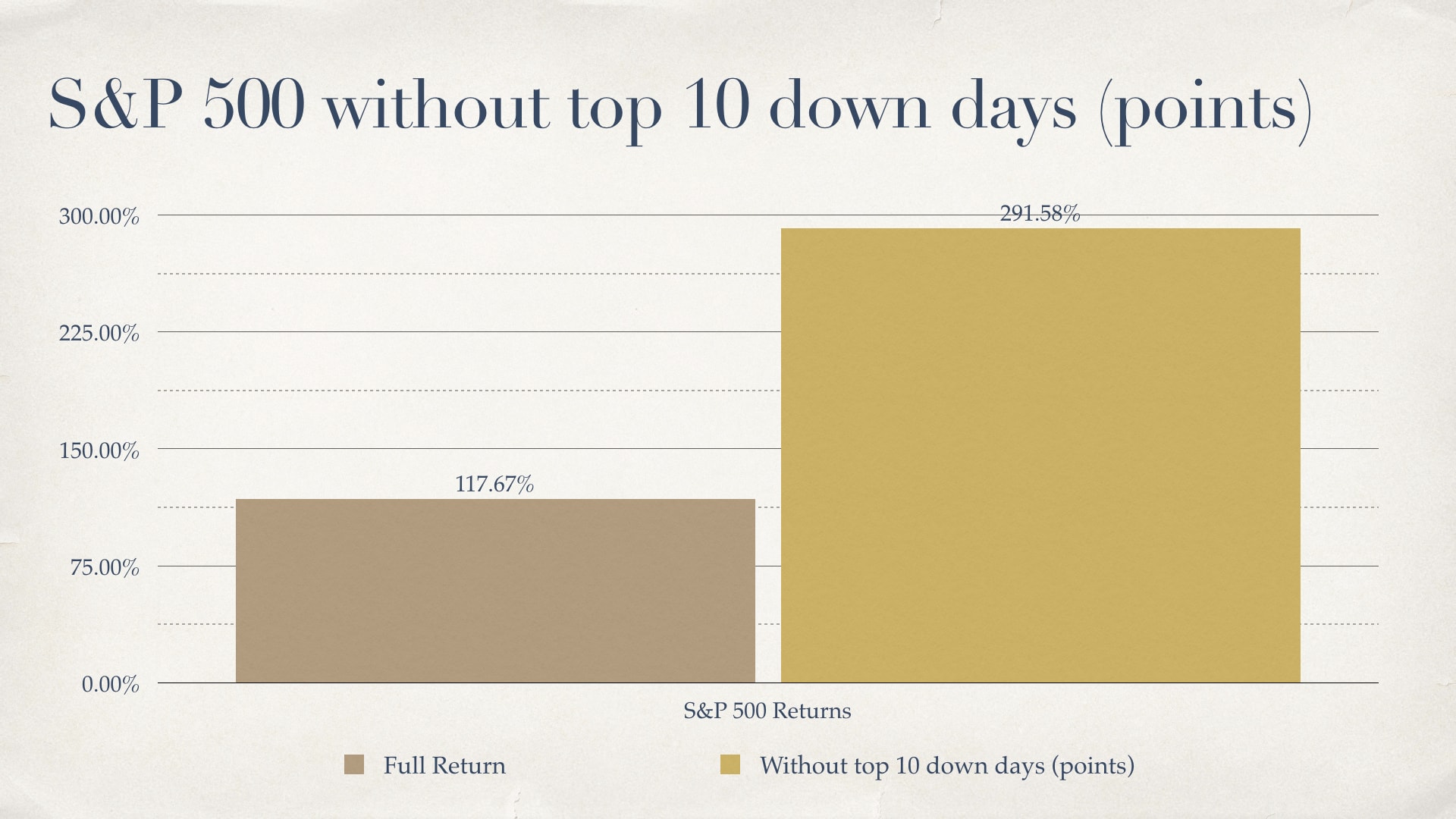

Although the bears shape the markets, they do not rule it, at least in the past 20 years. To prove our point, we’ll be simulating the S&P returns using those same 5,054 working days—to avoid skewed results—, however, instead of erasing gains we’ll be erasing the DOWN DAYS.

What a blessing. We’ll be ERASING from History, the top 10 largest daily point LOSSES, leaving just the fun.

| Rank | Date | Net Change (Points) |

| 1 | 2018-02-05 | −113.19 |

| 2 | 2008-09-29 | −106.62 |

| 3 | 2018-02-08 | −100.66 |

| 4 | 2018-10-10 | −94.66 |

| 5 | 2018-12-04 | −90.30 |

| 6 | 2008-10-15 | −90.17 |

| 7 | 2018-10-24 | −84.59 |

| 8 | 2000-04-14 | −83.95 |

| 9 | 2008-12-01 | −80.03 |

| 10 | 2011-08-08 | −79.91 |

If removing the top 10 up days from 20 years of data would’ve brought us misery, conversely, without the top 10 DOWN days, we would’ve been rich, right? 1,200% return? 3,000% return?

Yippee Ki Yay.

291.58% is all you would’ve got. Don’t get us wrong, it’s not that bad, 14.58% per year on average, 2.48 times more return. However, because we’re on the Extremistan World we were expecting, at least, to be Gods of Thunder.

Instead, we’ve slipped on a banana peel.

“Don’t forget who’s taking you home

And in whose arms you’re gonna be.

So darlin’, save the last dance for me”

Extreme events, bulls running, bears tearing victims apart, randomness, the failure of simple statistical methods, the smell of fear, what kind of place is this? Why take chances in a place like the financial markets?

Because we love it. The call for adventure is what we humans have in our blood, deeply marked in our DNA. Our soul has its own ancestors. We are lived by powers we don’t fully understand. The will to get somewhere must be greater than the pain we have to endure to get there. The goal is not the destination, but the path itself. That’s where the success lies.

We must face the Extremistan like the first explorers of the seas faced the almighty and mysterious oceans a long long time ago, during the so-called Age of Explorations, an era that would permanently alter the world. The brave men from Portugal, Spain, Italy, Great Britain, France, and the Netherlands, didn’t simply throw themselves into the oceans with canoes without any previous and meticulous planning. They were backed up by structure, methods, plans, complex systems and high doses of courage. 500 years later, here we are, exploring the deep space, planets, and sending space probes to face the unknown. And trading the financial markets as well.

That is why instead of just finishing this newsletter with a “nice to see you, until next time”, we’ve saved the last dance for you. In the second part of the Welcome to Extremistan series, we will be talking about how to survive and be successful in the Extremistan.

© 2019 Trading Justice. All rights reserved.