Menu

Trading Justice Newsletter

Trading Justice Newsletter

For him [Michel de Montaigne], the greatest problem with the law was that it did not take account of a fundamental fact about the human condition: people are fallible. A final verdict was always expected, yet by definition, it was often impossible to reach one that had any certainty. Evidence was often faulty or inadequate, and, to complicate matters, judges made personal mistakes.

No judge could honestly think all his decisions perfect: they followed inclinations more than evidence, and it often made a difference how well they had digested their lunch. This was natural and thus unavoidable, but at least a wise judge could become conscious of his fallibility and take it into account. He could learn to slow down: to treat his initial responses with caution and think things through more carefully. The one good thing about the law was that it made human failings so obvious: a good philosophical lesson.

If lawyers were error-prone, so too were the laws they made, since they were human products. Again, that was a fact that could only be acknowledged and accommodated rather than changed. This sideways step into self-doubt, self-awareness, and acknowledgment of imperfection became a distinctive mark of Montaigne’s thought on all subjects, not just the law.

Born in 1553, Michel de Montaigne was one of the most significant philosophers of the French Renaissance. The excerpt above was as valid in the 16th Century and it is now during the 21st.

People are fallible, even the ones in the high castle. The problem is that many use this as an excuse for not trying things.

Using your fear of failing as an excuse is OK if we are talking about things we can live without, like, for example, skating or surfing. Yes, I didn’t want to fail and splat my face on the ground or break an arm or, even worse, die while surfing a tsunami, like Bodhi, character played by Patrick Swayze in the 1991 American action film Point Break. That is why I never wanted to learn those things. OK, I can live with that.

How about investments, may I ask? Are you delegating your own financial future to someone else because you panic on failing?

That is what this month’s newsletter is all about. “The Omelet & The Eggs” is all about being afraid to fail in the financial markets and using it as an excuse to leave your money as it is, because “at least I am not losing anything”.

Yes, you are. You are losing a lot. Let’s move on.

“The Omelet & The Eggs” started with a casual conversation between me and a friend over WhatsApp. Although I am not sure this is applicable to all situations, we can learn a lot about investing in a conversation over instant messaging applications. I wish this conversation had happened live, preferably with wine, but it didn’t. Via WhatsApp with no alcohol was how it proceeded.

This friend of mine knows I’m a trader. She lives in Northeast Italy, in the Veneto area. I live in the North, Lombardia. We have almost the same background in life, coming from a family mostly composed of immigrants that arrived in Brazil in miserable conditions escaping from war, famine, and diseases in Europe.

Her family is from Poland, mine is from Italy. There, in Brazil, these hard-working people battled their way up in life. Our parents were also hard workers that still faced poverty and famine during childhood but finally moved our families to the middle-class extract.

We are also about the same age. She was born in 1979 and I was born in 1976. We have kids of the same age as well, both born in 2014. We’ve escaped Brazil for the same reasons too.

We first met in December 2003, during the pre-social network era. I was the bass player of a metal band and she was the guitarist’s girlfriend. We have been good friends ever since.

On that particular WhatsApp conversation, we began talking about money, building wealth, getting old and leaving a legacy behind for our future generations. She has this money, not huge amounts, although not too shabby either and she feels that something is wrong—or, at least, not right.

— ‘So, what’s your struggle?’, I’ve asked.

— ‘We have this money and we wanted it to grow. Not huge amounts but I think it is something.’, she replied.

— ‘Where is it?’

— ‘In the bank doing nothing there.’

— ‘I see. What are your goals? What do you want with this money?’

— ‘Just to make it grow. Build wealth. But I don’t want to lose! I’m terrified of losing anything! [giggle]’

(hmmm…)

— ‘Losing you already are, you see. The Eurozone is not growing, the Euro is not in good shape and inflation in Italy peaked at 1.7% last year. Interest rates are at the sub-zero mark and there is a default risk in the foreseeable future. Maybe Italy wants to follow Greece’s footsteps, who knows. Have you ever thought about opening an account in the US?’

(panic sets in)

— ‘IS IT LEGAL?? OMG!!’

— ‘Perfectly.’

— ‘But I don’t want to lose! I am terrified of losing, terrified of getting caught doing something illicit! I don’t wanna go to jail!’

— ‘Losing you already are and moving money to the US is not something illegal, I told you. OK, here’s an example. Take about –2% of your money every year. This is more or less how much you are already losing. If the situation degenerates you can add more to that loss.’

Then, the conversation proceeded, me arguing and she panicking. In short:

There is an old saying that goes like this: “paper money always returns to its intrinsic value which is zero”. Very true.

If you are one of the regular readers of this free newsletter, inflation is no stranger to you at all. The October 2018 edition was entirely dedicated to this topic, specifically hyperinflation.

By definition, hyperinflation “[…] is a macroeconomic event that occurs as a result of a steep devaluation of a country’s currency that causes its citizens to lose confidence in it. When the currency is perceived as having little or no value, people begin to hoard commodities and goods that have value. As prices begin to rise, basic goods — such as food and fuel — become scarce, sending prices in an upward spiral. In response, the government is forced to print even more money to try to stabilize prices and provide liquidity, which only exacerbates the problem.”

Thanks, Investopedia.

Hyperinflation is generally considered to exist when prices rise by more than 50% in one month. In a hyperinflationary environment, unlike in a low inflation one, we see a rapid and continuing increase in the cost of goods, and also in the supply of money. This creates a vicious circle, requiring ever-growing amounts of new money creation to fund government deficits. When a government doesn’t have money, it’s hard to resist the unbearable temptation of hitting the rolling press PRINT button.

There is an old saying that goes like this: “paper money always returns to its intrinsic value which is zero”. Paper money is our money referred to as fiat currency in technical jargon.

Fiat currencies are depreciating assets by nature, with no intrinsic value. They are established as money by a government or central bank regulation. Simply put, our money only has value because the government maintains its value.

Or not.

This is where hyperinflation kicks in.

— ‘That will never happen to the US’, someone might argue.

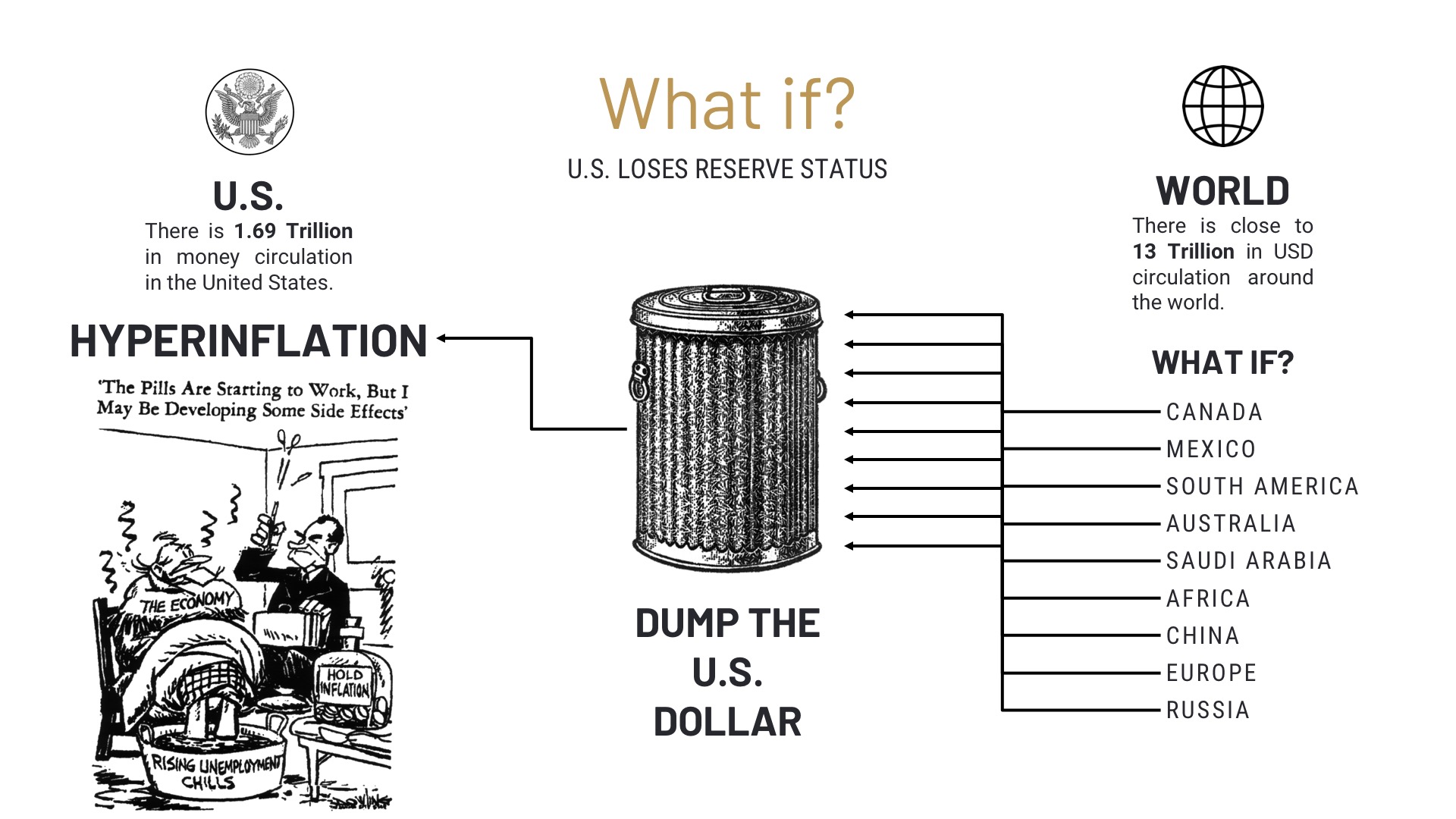

It’s not because the United States didn’t experience such a case that it won’t happen in any capacity. Some people use History as a warning, while others are more inclined to use it as a manual, a guideline on how to proceed in the present and plan the future.

Notice how steep the U.S. Dollar devaluation becomes short after the creation of the Federal Reserve (1913). In 1971, Richard Nixon put the final nail in the coffin, ending the gold standard, burying the Bretton Woods pretty deep, making the U.S currency a full-fledged fiat currency worth ZERO in terms of intrinsic value.

The complete collapse of the U.S. Dollar is not a matter of IF but WHEN. Here’s another terrifying infographic:

What about the Euro?

The same principle applies to the Eurozone. I didn’t send this next chart to my friend but I can sure share it here with you.

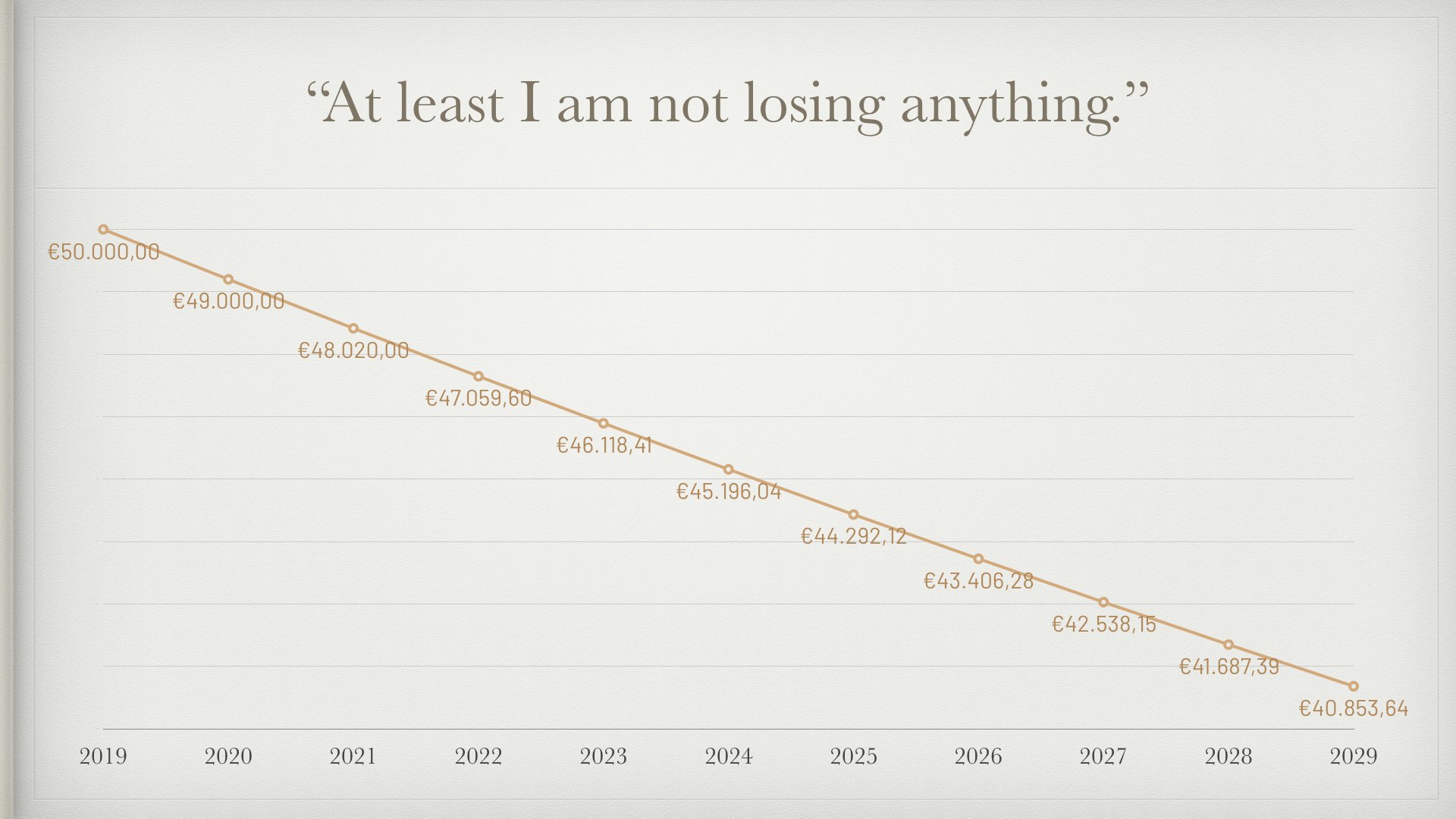

Inflation is an invisible tax. “My money is in the bank doing nothing. At least I am not losing anything”. Yes, you are.

Let’s say she has some €50,000 in a bank account. The graph simulates a –2% annual corrosion in the purchasing power of her hard-earned money. Pretty close to the inflation rate in Italy in 2018. In 10 years, something like €10,000 will be forever gone. Almost €1,000/year. When we were kids, the inflation rate in Brazil was 30,377% per year (1990). When I was 10 years old, in 1986, one of the highlights of my daily routine was to go with my two brothers and my mother to the supermarket after school to patiently stand on huge lines just to buy some eggs, meat, and milk.

My friend wants the omelet but is afraid of breaking the eggs. Meanwhile, the eggs deteriorate in the refrigerator. That is exactly the point here.

Elon Musk hates taking weeks off. Me too. I am not comparing myself to Elon, let me be totally clear on that. He is way more intelligent and rich than me, I know my place in the world, but when it comes to vacation, dude, we can high-five. Here’s an interesting bit I found on CBC:

“In addition to working all the time, Musk—who says he has only tried to take off a handful of times—has had terrible luck when it comes to vacations. In 2015, Musk said that he had only taken off twice in more than a decade, and both times were problematic.”

“The first time I took a week off, the Orbital Sciences rocket exploded and Richard Branson’s [Virgin Galactic] rocket exploded in that same week. The second time I took a week off, my rocket exploded. The lesson here is: don’t take a week off.”

I don’t have rockets to explode, just my patience, which does just the same. But that is not the point here.

Have you noticed how much time people spend planning their next family trap, I mean, trip? It can take months. A 1-week trip in August begins in January. Do you think I am kidding? My wife is already planning next year’s vacation. My friend, the epicenter of this newsletter, loves to go to the USA and spend a whole month there. By the end of the trip, she already has the next trip planned out.

Now, try to ask these people about their money. Net worth. Retirement. Legacy? Investments? … Anyone?

Nothing.

They want to make every trip cost-efficient, which means, the most fun they can get for every dollar spent even if it takes a whole month to plan one week. You won’t have 5 minutes of their attention to plan out their future and the future of their kids, though.

Wrong priorities? Instant gratification? God knows. The fix is easy, though:

There you go. Instead of ‘Vacation’, you have ‘Investing’.

I totally understand my friend though. People hate to lose money and the stock market is the place where it can happen in all its glory. Inflation corrodes money too but it is invisible. “If I can’t see it, it doesn’t exist.”, they might think.

Let me ask you something: Have you ever experienced that awkward situation on a family dinner or a meet up at your friend’s when someone throws this ball to you?

— “Did you know that the stock market is a place where you can lose all your money?”

If you are a trader and/or an investor, even a beginner, you know that there is only one possible answer to this question. Precisely this one:

— “It sure is.”

Whoever asked you that is absolutely right. The stock market is THE place to lose your shirt. There is also Las Vegas or getting yourself involved with the Italian Mafia but we are not covering these in this newsletter.

Have you ever took some time to read Tackle’s disclaimer?

“All investing and trading in the securities market involve a high degree of risk. […]”

If we love the markets so much why don’t we hide this type of message so we can attract people like my friend and my wife? Because risk is part of our job, not a thing that we should feel ashamed of. Traders and investors trade risk, uncertainty, and randomness because they’ve learned to do so. If these are fully suppressed, so is trade and investing themselves. What’s the point, then? These are the actual things that will make us money in the long run.

The problem is that the person who asked you doesn’t know anything about it. They have the DNA of the prudent investor: Do Nothing Approach. They think that parking money in a mutual fund and sitting on their hands will help them build wealth.

So, while the stock market is rated ‘NC-17’ due to its explicit downside risk, the “safe and prudent” funds with their unnamable diversified holdings and obscene fees are rated ‘G’.

The promise of a full return with no apparent risk? We pass. That’s not part of the investors’ DNA and this is what we have to teach people.

Imagine one day I wake up and find this message on my WhatsApp:

— “I’ve decided to follow your suggestion. I will invest! I am so happy!”

Before I even brush my teeth I am already smiling.

— “I’ve sat down with my bank account manager and she suggested this fund that is composed of government sovereign bonds and corporate bonds from all over the Eurozone. No risk, no volatility, she guaranteed to me.”

“The dream is over”, as John Lennon once said.

You see, there is a natural conflict of interest here. The bank account manager got one job: to put meat on her family table. I got nothing against that, I want to be clear. The problem is that the system’s structure is conflicted by nature. She is not interested in my friend’s future, just in selling the fund that is most profitable to herself. Fees—which are quite obscene, by the way—is what matters, to the extent that she ends up handing my friend a wrong map. As so wisely stated by Nassim Taleb “Giving someone the wrong map is worse than giving them no map at all”.

If you want to build your wealth, take care of your finances and leave a legacy to your heirs all you need is money (obviously), a strong commitment, a good dose of patience and discipline and a mind of steel. After all, we are talking about your future and the future of your family as well as the following generations. That is something that cannot be taken lightly. It’s not irrelevant or futile either.

Allow me to present some arguments for you.

“Beneath your mask of logic, I sense a fragility. That worries me. Steel your mind, Holmes.”

— Lord Blackwood to Sherlock Holmes in the movie Sherlock Holmes (2009)

Solving Lord Blackwood’s crimes were only possible because Sherlock steeled his mind and did not fall prey to all the hocuspocus and mise-en-scène smartly used by Blackwood to impress his victims and enemies. The stock market will use the same tricks against you. It is the biggest money transfer machine (after Las Vegas, I guess): it transfers money from the inpatient investor to the patient one, from the undisciplined to the disciplined one, from the distracted to the focused one, from the lazy to the diligent one.

My friend’s counter-argument could be: “I am invested in zero-risk fund, do you remember?”

Parking your hard-earned money on a fund that rips you in half with obscene fees, one that delivers horrible returns and, additionally, is labeled zero-risk, will certainly qualify you as inpatient and/or undisciplined and/or distracted and/or lazy. Steel your mind so you won’t fall prey to all the hocuspocus and mise-en-scène of your bank account manager.

In the video “Warren Buffett’s First Television Interview – Discussing Timeless Investment Principles”, when asked what did he consider the most important quality for an investment manager, Warren shoots:

“It’s a temperamental quality, not an intellectual quality. You don’t need tons of IQ in this business. I mean, you have to have enough IQ to get from here to downtown Omaha but you do not have to be able to play three-dimensional chess or be in the top leagues in terms of bridge playing or something of a sort. You need a stable personality. You need a temperament that neither derives great pleasure from being with the crowd or against the crowd. Because this is not a business where you take pools, it’s a business where you think and Ben Graham would say that you’re not right or wrong because a thousand people agree with you. And you’re not right or wrong because a thousand people disagree with you. You are right because your facts and your reasoning are right.”

The mindset is the cornerstone of any successful investment endeavor. You don’t need any extraordinary math skills or the highest IQ to invest your money. You just have to be in the center. Neither falling off of a cliff when you lose, neither popping champagne on every single winning. Stable. Serene. The discipline of a Shaolin monk. The spectator of your own ego.

Again, if you parked your money on a horrible fund like my friend did and you are actually able to keep your zen even knowing that this was the worst thing you could have done, you already have the temperamental quality need, you’re just invested in the wrong vehicle.

“See, there’s two kinds of doctors. The kind that gets rid of their feelings. And the kind that keeps them. If you’re going to keep your feelings, you’re going to get sick from time to time. That’s just how it works.”

That’s Dr. Mark Greene, the fictional medical doctor from the television series ER, portrayed by the actor Anthony Edwards.

Have you ever tried to play jokes with a doctor, especially those inside emergency rooms? They are robots and they don’t joke around. Do you know why? Because they can’t. Emotions are like breaches that weaken their fortresses. The life or death of many patients lies in their hands.

All they run inside them are systems. They can’t and must not get involved with their patients, otherwise, they won’t run their systems properly and this could mean losing a human life, or an animal, in case of veterinarians.

They see the patient, understand the case and run the system. What to do, how to do, when to do, who should do what, what medications to give in what dosage, what procedures to make. And that’s it. How did they reach that point? Training and discipline.

There are also two kinds of investors: The kind that gets rid of their feelings and the kind that keeps them. If you’re going to keep your feelings, you’re going to get sick from time to time. That’s just how it works.

Be like emergency doctors when running your investments.

“Investing should be more like watching paint dry or watching grass grow. If you want excitement, take $800 and go to Las Vegas.”

—Paul Samuelson—

Paul was an American economist, considered by many the Father of Modern Economics. He was also the first American to win the Nobel Memorial Prize in Economic Sciences.

Investing should be more like watching paint dry, or watching the grass grow or even the witnessing water evaporate and less like than riding a rollercoaster.

Now that you have steeled your mind, you have the temperamental quality necessary to invest and you are feeling strong as an emergency doctor, let’s invest.

Oh, so you don’t feel confident yet? Read the next session, then.

The three arguments presented could be used by you against me. If you want to do so, they should work as solid evidence as to why you should even try to learn to invest:

It won’t work.

I don’t know.

It doesn’t make sense.

I can’t do this.

I’m not good at this.

I don’t get it.

However, as I mentioned at the beginning of this article, taking care of your future is not like learning how to surf or how to skate. Taking care of your finances and setting the foundations for a prosperous future for you and your family is not something that, if not accomplished, will make you feel good about yourself. I bet you won’t even sleep thinking about it.

In the book, “Mindset: The New Psychology of Success”, Carol Dweck does a thorough and detailed dissertation on the two types of mindsets we humans have: the fixed mindset and the growth mindset.

According to her, people with a fixed mindset believe that their qualities are carved in stone. They think they have only a certain amount of intelligence, urging to prove to themselves and to others that they are smart enough. Will I succeed or fail? Will I looks smart or dumb? Will I feel like a winner or a loser?

In a fixed mindset, everything is about the outcome. If you fail, it’s all been wasted. Failure defines you. When it comes to investing, the mindset will look more or less like this:

— “OK, I will learn how to invest and when I do it has got to be perfect. My goal is to quickly build my wealth. I won’t lose money, I will make no mistakes. It will be effective, and efficient.”

If we are talking about breaking eggs to make an omelet and you have never done it before, it is almost certain that your first mistake will happen while breaking the eggs. If you pass this phase, you will most certainly put too much salt and seasoning, or maybe burn the omelet or, even worse, destroy it while trying to flip it on the frying pan.

Does that mean you won’t be ever able to cook a delicious omelet in the near future? Not at all.

Now replace omelet with investing. You get the point. This leads us to the second type of mindset.

The opposite approach to the fixed mindset is the growth mindset. It is based on the belief that your basic qualities are things you can cultivate through your efforts, your strategies, and help from others. To these people, everyone can change through application and experience.

In this mindset, the path is more important than the outcome. It allows people to value what they’re doing regardless of the outcome. These people tackle their problems, work on important issues and chart their courses. Failure is just a possibility, not a definition of what they are.

In the 90s, the self-esteem movement took over the world and started a new norm: everyone became brilliant overnight. This led to the acceptance of mediocrity instead of excellence producing entire generations of people who are afraid of challenges and criticism.

As investors, if every time you err you either define yourself as a complete failure or you pat yourself in the back thinking you are an uncomprehended genius, your career won’t last long, sorry. Bad decisions you make can destroy your wealth once and for all. If most people were raised and still nurture the fixed type of mindset, then the self-esteem movement provided a hard and definitive blow against it.

There is a way out of this trap, however.

Begin nurturing a growth mindset. The first step you can take towards it is:

(1) avoid praising your efforts during a failure and

(2) avoid bashing yourself like you are the worst creature to ever walk the face of this planet.

The extremes do not work as previously mentioned.

The second step—the middle ground—is to identify the mental triggers that lead you to fail so you can overcome them one by one. It doesn’t have to be complicated; something simple like the list cited above will get you started:

This doesn’t work.

I don’t know.

It doesn’t make sense.

I can’t do this.

I’m not good at this.

I don’t get it.

Now, let’s attach the word YET to the end of each phrase and see how it works:

This doesn’t work…yet.

I don’t know…yet.

It doesn’t make sense…yet.

I can’t do this…yet.

I’m not good at this…yet.

I don’t get it…yet.

The growth mindset, the thriving in the face of failure, starts with one word. One word, a world of difference.

“Investing is the intersection of Economics and Psychology.”

—Seth Klarman—

Learning how to trade, how to read a chart, the basics of technical analysis and chart patterns, learning how to read corporate statements and prepare your portfolio for earnings season, learning options strategies and advanced hedging techniques, or learning how to operate the brokerage platform, these are all pieces of cake that you can swallow with little to no effort. It can be intimidating when you’re new but trust me: barking dogs seldom bite.

Learning how to control your emotions when you get the max loss on some of your stock positions or witnessing your portfolio as a whole melting some –50% right in front of your eyes and still keeping your zen intact, that is a whole different animal to swallow and digest.

The more you know, the more there is to know. New investors are eager to learn and make money, but that’s just not how it works.

Would you trust a doctor who learned his craft just by reading books? The learning curve you’ve got to submit yourself to in order to become a skilled physician is tremendous. Reading books is just a part of it. Practice is king and the total control of the emotions is paramount.

It is no different in the financial markets. It will take years of reading, learning and practice for you to become a successful investor. However, once you adopt the right mindset and the necessary discipline, the results will appear right away.

The stock market is like a madhouse and new technologies only leverage such madness. Don’t go crazy with it. Be the person on the outside looking in.

Being hungry and foolish all the time is good but the pace should be steadfast. Remember that in this journey, speed does not matter, direction does. Bear in mind also that there is no finish line but there is certainly a starting one. Start now. Break the eggs, don’t let them deteriorate in the refrigerator. Enjoy the journey of making omelets.

Keep walking towards the light but don’t try to outpace it. The problem of being faster than light is that you can only live in darkness.

© 2019 Trading Justice. All rights reserved.